English

English Español

Español Français

Français Deutsch

Deutsch Italiano

Italiano Português

Português

“A change that becomes self-perpetuating and accelerates decarbonization regardless of factors like politics or policy reversals” has been coined as a “global tipping point” by climate scientists like Tim Lenton of the University of Exeter.

Lenton observes that solar photovoltaic electricity is now 1.5-2.5 times cheaper than gas and 2-3 times less expensive than coal in key markets such as the US and China. India and Germany. Solar PV is the most cost-effective energy source for electricity production and will dominate the market, reaching an estimated 50 percent of global production by 2050. It adds jobs and reduces air pollution (Global Tipping Points, 2025). The US will continue to add solar capacity. The pace will slow as tax credits are phased out but could accelerate again when Trump leaves office. Cumulative installed solar capacity has grown from 200 GW in 2015 to 1900 GW in 2024.

A second tipping point, also shared by Lenton, is the use of heat pumps that are already less expensive than boilers in leading markets. Reversible heat pumps also provide air conditioning. The global heat pump market is projected to reach USD 130 billion by 2030, from an estimated USD 83 billion in 2025, with a 14 percent annual growth rate. Today, heat pumps are at the forefront of renewable energy solutions. Innovations such as hybrid systems, integration with solar panels, and the use of AI for optimizing energy efficiency are shaping the future of this technology. They will play a crucial role in decarbonizing residential, commercial, and industrial heating and cooling systems.

The use of battery electric vehicles (BEVs) is the most effective way to decarbonize passenger road transport. A first tipping point has been crossed in the leading markets of China and the EU, where the cost of purchasing and operating a BEV is less than that of a fossil-fueled car. A shift in consumer preferences occurs when the parity of purchase price is reached.China, due to decades of investment in EV production, achieved price parity as early as 2022 (Global Tipping Point, 2023). The number of electric cars in use has been growing steadily, reaching 58 million last year, with more than half in China and 17 percent in the EU. Norway, with a combination of progressive policies and incentives, has achieved a record penetration of EVs, comprising 90 percent of new car sales in 2024.

A fourth tipping point is the reduction of the costs of climate damage through adaptation. The property and casualty insurance, with global premium payments of $2.4 trillion last year, is the first to be impacted. Initially, this will result in higher premiums or policy cancellations. In the US, between 2021 and 2024, home insurance rates have risen 27 percent nationally. The State of California gave State Farm Insurance permission to raise rates 17% in the wake of the 2025 wildfires. The growing insurance availability and affordability crisis is no longer limited to particular coastal states but is spreading rapidly across the country, including the Midwest and the so-called climate havens (Stancil, 2025). Without insurance a homeowner cannot obtain a loan. Without a loan, many homes will not be built.

This phase will be followed by a more holistic approach where insurers offer discounted premiums when preventive measures are taken, such as building flood walls. Investing in structural upgrades, such as storm shutters, raised foundations, or fire- and hail-resistant roofs, will be necessary to obtain insurance and reduce costs. Adaptation, already 29 percent of total climate investments (see below), will continue to accelerate.

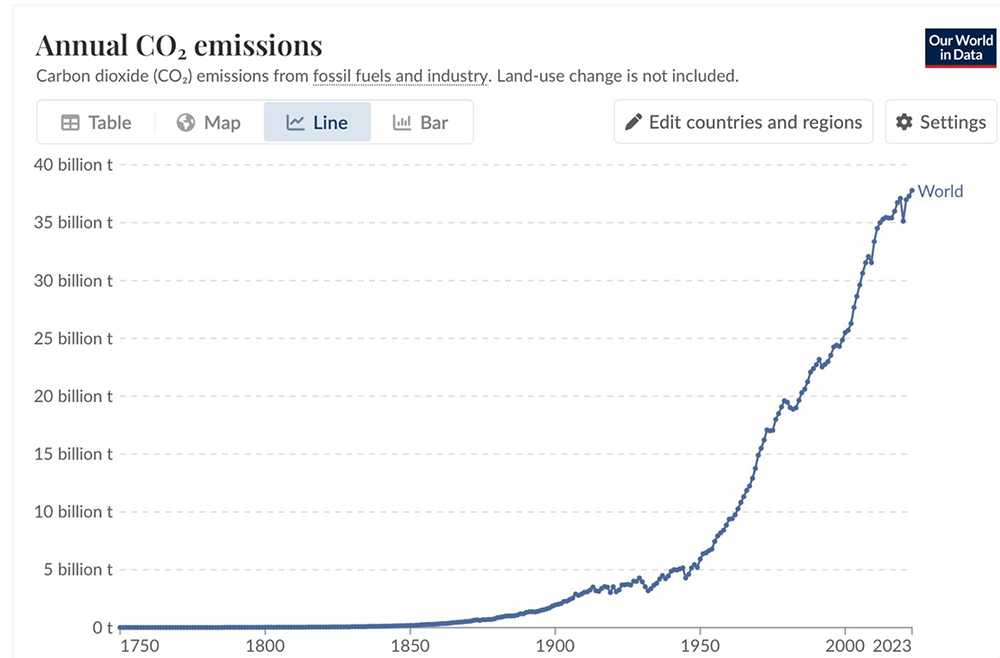

Unfortunately, these tipping points are not yet sufficient: carbon emissions from fossil fuels continue to outpace improvements.

In the last few years, the growth of global CO₂ emissions has slowed, but it has continued to rise. Coal, one of the worst emitters, still accounts for 45 percent of the total contribution from fossil fuels.

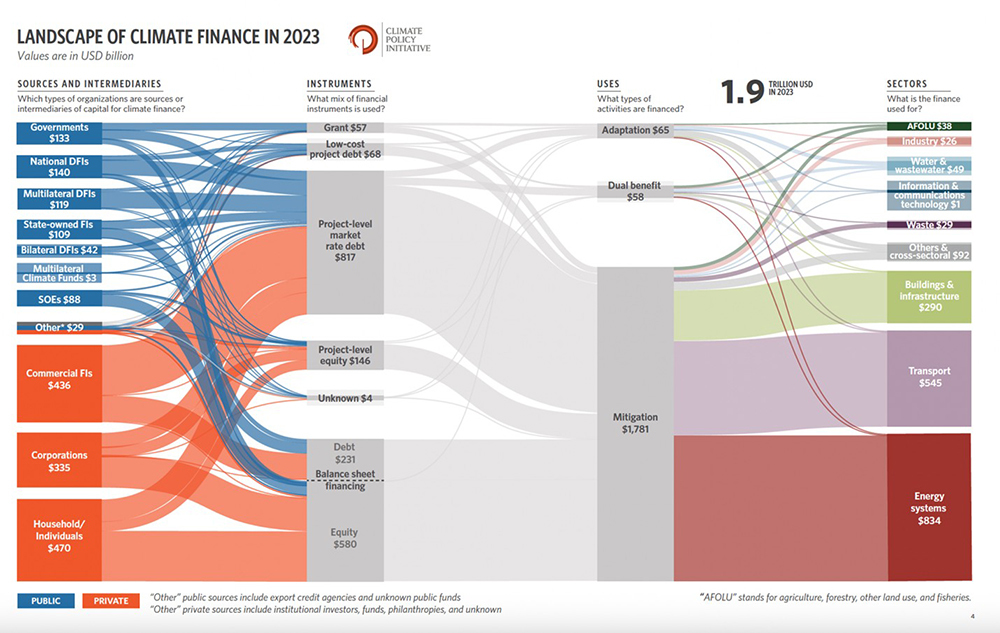

This highlights the importance of funding to improve the climate. The latest data concerning climate investments has been reported. For the year 2023, the total was USD 1.9 trillion.

Two-thirds of the funding came from the private sector, 22 percent from public domestic financing, and 10 percent from public international sources. Within the private sector, households/individuals made the most significant contribution of USD 470 bn (38%), followed by the commercial financial institutions at USD 436 bn (35%), and by corporate investments of USD 335 bn (27%) (Naran, 2025).

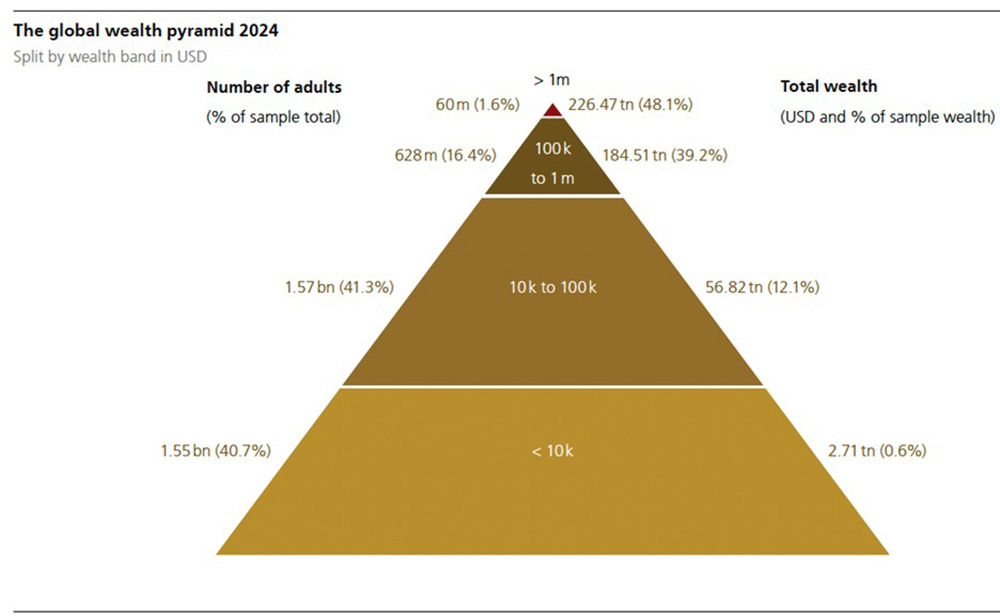

In general, the wealth of individuals/households is closely followed by investment banks for funding opportunities. For 2024, UBS has estimated the global wealth of households/individuals, shown as a pyramid (UBS, 2025).

Source: UBS.

Source: UBS.

Considering the top two wealthiest categories (with wealth of $100,000 and above), their total wealth is $411 trillion.

UBS also reports that growth in individual/household wealth has accelerated to 4.6 percent in 2024 from 4.2 percent the previous year. At this rate, the annual increase in the top two categories of wealth was $19 trillion in 2024, a significant amount.

How does this compare to climate investments? As reported, the global amount was $1.9 trillion in 2023, and the shortfall in climate investments to meet the 1.5°C schedule of the Paris Agreement is about $7 trillion annually up to 2035 (UN, 2025). As recently illustrated, costs in the 1.5°C scenario, compared to the business-as-usual projection, are 54 percent less ($1,300 tn) from 2025 to 2100 (Mebane, 2025).

The required additional investment, $7 trillion, is 37 percent of their annual wealth increase.

Would these wealthy individuals be willing to forgo about one-third of their annual growth? No, the immediate reaction is to maximize short-term growth. Is it in their best interests to do so? Yes, losses will be much less.

The wealthiest households/individuals should consider insuring their capital. The best insurance is promptly realizing society’s climate goals and investing part of their wealth growth in climate improvements. How this could be enacted will be the subject of a subsequent article.

From a moral perspective, we recall that the most affluent nations, and their wealthy citizens, have contributed the most to cumulative carbon emissions.

References

Global Tipping Points, (2025), ‘New Solar Photovoltaic Cheaper Than Coal and Gas Globally’, Global-tipping-points site.

Global Tipping Points, (2023), ‘Crossing the Tipping Points: Case Studies Electric Vehicle,’ Global-tipping-points site.

Naran B., et al. (2025), ‘Global Landscape of Climate Finance 2025’, June 23, Climate Policy Initiative.

Mebane, W. (2025), ‘Neglecting Climate Investments’, August 10, Meer.

Stancil, K., Fabian, C. (2025), ‘Mapping the Home Insurance Crisis’, Public Citizen, April 24.

UBS, (2025), ‘Global Wealth Report 2025’.

UN, (2025), ‘Emissions Gap Report 2024’.