English

English Español

Español Français

Français Deutsch

Deutsch Italiano

Italiano Português

Português

A clarification for those not familiar with climate terminology is necessary. By 2100, the world's average surface temperature should rise to no more than 1.5 °C (2.7 °F) warmer than pre-industrial levels. The 1.5 C threshold was the target established in the Paris Agreement of 2015, a treaty in which 195 nations pledged to tackle climate change. In a 1.5C world, many of the deadliest effects of climate change are reduced. To achieve this, by 2050, the world should be producing only a small amount of greenhouse gases, equal to the amount we could remove by other means, so that the net emissions would be zero. On this basis, the investments necessary to mitigate the emissions are calculated.

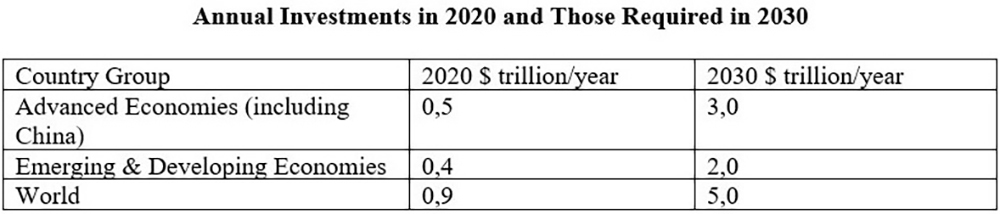

According to the IMF, “the path to net zero by 2050 requires low-carbon investments to rise from $900 billion in 2020 to $5 trillion annually by 2030. Of this figure, emerging and developing countries (EMDEs) need $2 trillion annually, a fivefold increase from 2020. Even if advanced economies meet or somewhat exceed their promise to provide $100 billion a year, the bulk of the financing for these low-carbon investments will need to come from the private sector.” (Black, p. 1, 2023).

Let us look at the international context regarding the gross domestic product and population. As illustrated below, each group's population is roughly 4 billion people. Still, the GDP is 10.6 times higher in advanced economies (including China) than in emerging and developing countries. The GDP per capita in the emerging and developing economies (EMDEs) is only 10 percent of that of the advanced economies.

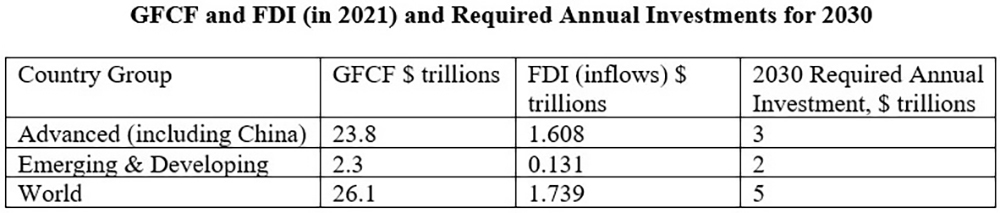

The gross fixed capital formation (GFCF), better known as investment, and the inflows of foreign direct investments (FDI), both for 2021, are compared to the 2030 annual required investments to meet the net zero by 2050 scenario.

For the advanced economies, the required 2030 investment of $3 trillion annually is 13 percent of the existing GFCF. The required annual investment can be obtained by growth in the current amount of GFCF and substitution of investments for clean energy investments in the current mix of GFCF investments. It is a challenging but feasible task.

Instead, the opposite is the case for emerging and developing countries. The required new investments are 87% of their total current GFCF. The level of green investments in these countries, 0.4 trillion, would have to be increased fivefold by 2030. Similarly, FDI would have to be greatly expanded to play a significant role. The special fund of 0.1 trillion to be contributed by the advanced economies is only five percent of the needed amount.

Reaching the 2030 mitigation investment goal at 1.5 C for emerging and developing economies will be very difficult, if not impossible.

As if the extraordinary amount of investment required was not enough, there are other significant obstacles:

- High inflation and accompanying interest rates discourage green investments that require more investment initially. In this situation, which is more frequent in developing countries, fossil fuel investments can be more profitable and easier to realise with lower upfront costs.

- There is greater risk of undertakings in EMDEs. Managerial experience is less, and the regulatory environment is unstable. Almost all developing countries lack the investment-grade credit ratings that institutional investors often require.

- Given the greater difficulties of operating in these countries, new mitigation projects are lacking. The competition for limited public funding is intense.

- The underlying moral dilemma of climate warming being caused initially by emissions from advanced economies discourages emerging and developing countries. They resent this, and at the same time, much of the climate damage is forecast to occur in their economies, particularly in low-lying areas.

This situation of the emerging and developing economies is a global problem and is certainly of concern to the advanced economies, subject to the cost of a warmer climate. Several decades ago, with fewer climate disasters and less vulnerability, advanced countries were less prone to weather and climate disaster costs. For example, according to the National Oceanic and Atmospheric Administration, in the broader context, the total cost of US billion-dollar disasters over the last five years (2018–2022) is $595.5 billion, with a 5-year average of $119.1 billion, the latter of which is nearly triple the 43-year inflation-adjusted annual average cost. The US billion-dollar disaster damage costs over the last 10 years (2013–2022) were also historically large: at least $1.1 trillion from 152 separate billion-dollar events.

The number and cost of weather and climate disasters are increasing in the United States due to a combination of increased exposure (i.e., more assets at risk), vulnerability (i.e., how much damage a hazard of given intensity—wind speed or flood depth, for example—causes at a location), and the fact that climate change is increasing the frequency of some types of extremes that lead to billion-dollar disasters.” As the example illustrates, advanced economies are increasingly vulnerable, exposed, and experiencing a growing frequency of extremes due to climate change. No country is a safe island.

The EMDMs have populations and economies growing faster than the advanced nations, with high potential carbon emissions and, therefore, substantial mitigation requirements (2 trillion dollars per year by 2030). The world cannot get to net zero without adequate EMDM mitigation.

If mitigation efforts are delayed, the annual investment targets will be reduced, but EMDM adaptation requirements and costs will increase. Furthermore, without adequate protection, potential damages and losses in GDP growth can be more than ten times higher than adaptation investments (Standard Chartered, 2023). Delaying mitigation will result in higher total costs.

The IMF projects that growth in public investment in EMDMs will be limited and that the private sector will, therefore, need to make a major contribution towards the significant climate investment needs of emerging and developing economies. The private sector will need to supply about 90 percent of the required investments. (Anandakrishnan, 2023).

The Fund recommends programmes aimed at strengthening macroeconomic fundamentals, deepening capital markets, and improving governance as a fundamental part of the EMDM policy mix. “Innovative financing, such as blended finance and securitization instruments, should be employed to initiate a managed phase out of coal power production... More extensive public-private risk sharing is critical to fostering climate-sensitive private investments in emerging markets and developing economies. Multilateral development banks and donors can play an important role in supporting blended finance, including through a more extensive use of guarantees.” (Anandakrishnan, p. 2, 2023). Collaboration with international firms that have successfully implemented programmes of energy efficiency, renewable electricity production, electrical infrastructure, electric vehicles, or heat pump production should be facilitated. The local markets and opportunities are to be fully explored. For example, electric vehicle production may differ, emphasising smaller vehicles and possibly local production.

As an individual investor in advanced economies, I desire a market that offers me all the possibilities to invest. An exciting opportunity is the creation of more impact-oriented investment portfolios that allow retail and institutional investors to finance such needed climate projects. These would differ from the popular ESG funds that make investment decisions based on environmental, social, and corporate governance factors that do not necessarily focus on climate issues. Giving individuals the choice of investing in mitigation and adaptation solutions where they are needed is part of this general strategy of allowing markets to work for climate change.

The assets under management by financial firms, such as Blackrock, are enormous. According to the Sovereign Wealth Fund Institute, the top 100 asset managers had almost $57 trillion of assets under management at the end of 2022. They could become key players in creating a variety of new financial instruments under their management. For example, institutional investors like pension funds may be interested in climate investments in advanced and EMDM economies. ETFs and mutual funds dedicated to climate improvements in EMDMs are additional possibilities.

In conclusion, advanced and emerging countries must work together to reach net zero, facilitating investment in emerging economies. The moral conundrum is that, on the one hand, the advanced economies are responsible for a large part of the initial carbon emissions and that, in particular, the US oil and gas industry is responsible for decades of delaying climate action; on the other hand, a significant part, approximately 40 percent, of the necessary mitigation is in the emerging economies with limited financial resources.

This problem can only be resolved by the advanced economies enabling investment in the emerging ones. Advanced economies alone will fail. Together, we can succeed.

References

1 Emerging Economies Need Much More Private Financing for Climate Transition.

2 World Needs More Policy Ambition, Private Funds, and Innovation to Meet Climate Goals.

3 2022 U.S. billion-dollar weather and climate disasters in historical context.